March 2026 Residential Activity in St. John’s Down 20.2% Compared to March 2025!

See below for full details on the St. John’s and province-wide housing market for March 2026 with comparative numbers for March 2025

Sales:

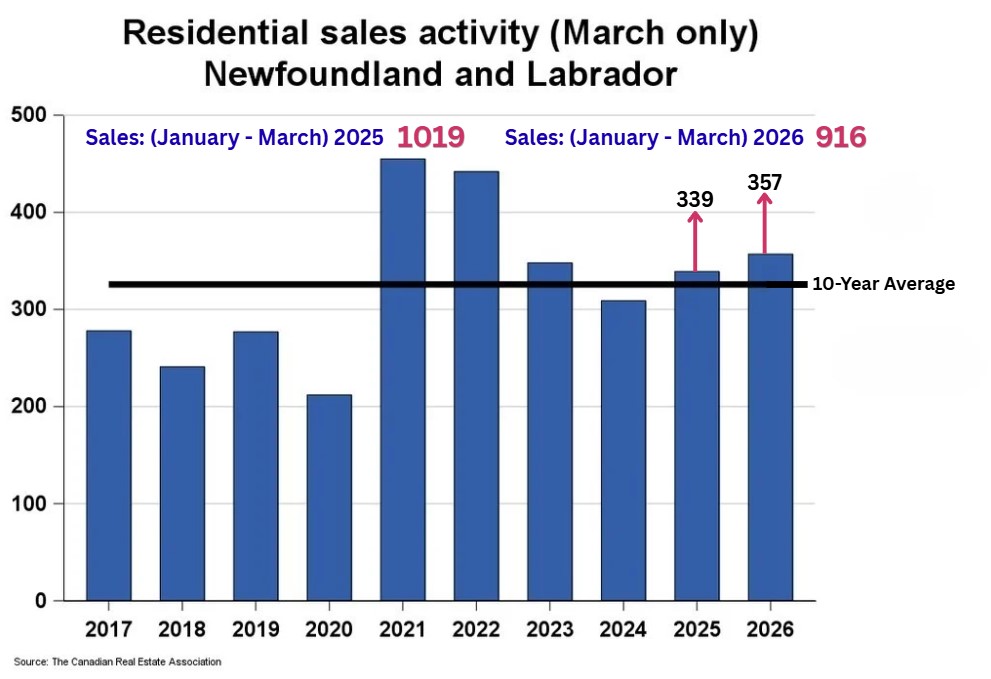

357 homes sold through the MLS® System of the Newfoundland and Labrador Association of REALTORS® in March 2026. This was an increase of 5.3% from March 2025

Home sales were 0.6% below the five-year average and 9.6% above the 10-year average for the month of March.

On a year-to-date basis, 916 homes sold over the first three months of the year. This was a large decline of 10.1% from the same period in 2025.

March Statistics For St. John’s Only

Residential activity in St. John’s saw a substantial decline of 20.2% on a year-over-year basis in March, while activity in the rest of the province posted a gain of 20%.

Single detached home sales in St. John’s were down sharply by 32.7% from levels recorded in March 2025.

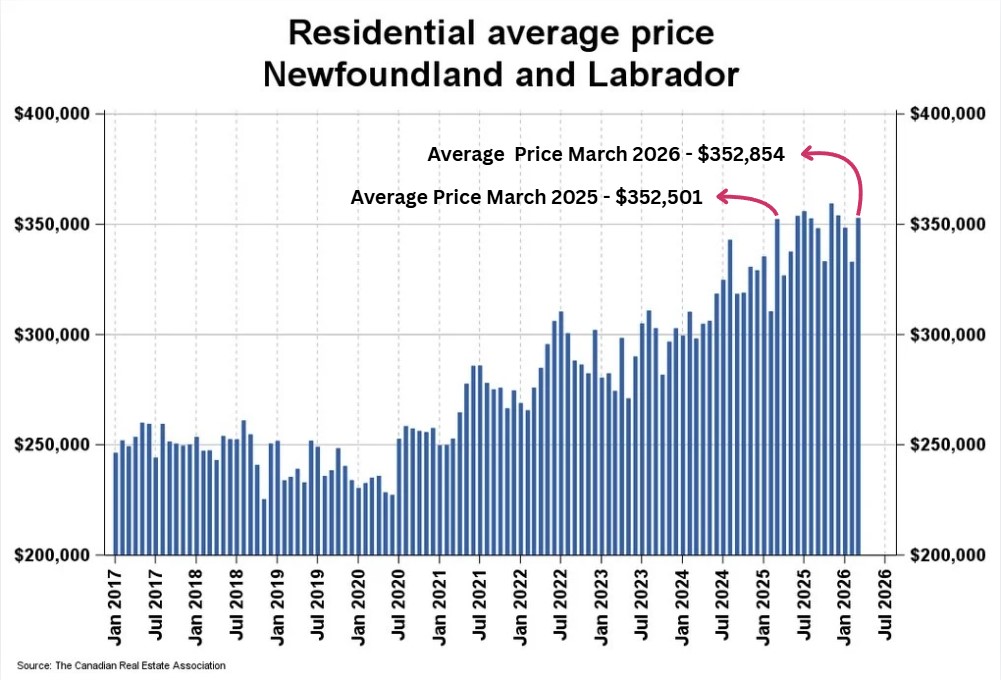

Average Price:

The MLS® Home Price Index (HPI)* tracks price trends far more accurately than is possible using average or median price measures.

See the end of the post for an explanation of the HPI.

The overall MLS® HPI composite benchmark price was $334,000 in March 2026, an increase of 9.3% compared to March 2025.

The benchmark price for single-family homes was $336,900, a moderate gain of 9.5% on a year-over-year basis in March. By comparison, the benchmark price for townhouse/row units was $302,300, increasing by 2.3% compared to a year earlier, while the benchmark apartment price was $253,800, up only 0.5% from year-ago levels.

March Statistics For St. John’s Only

The overall MLS® HPI composite benchmark price for homes in St. John’s was $393,500 in March 2026, increasing by 7.8% compared to March 2025.

The benchmark price for single-family homes in St. John’s was $412,000, a gain of 8.3% on a year-over-year basis in March. By comparison, the benchmark price for townhouse/row units was $297,300, up modestly by 3.8% compared to a year earlier, while the benchmark apartment price was $252,900, essentially unchanged, up just 0.6% from year-ago levels.

New Listings:

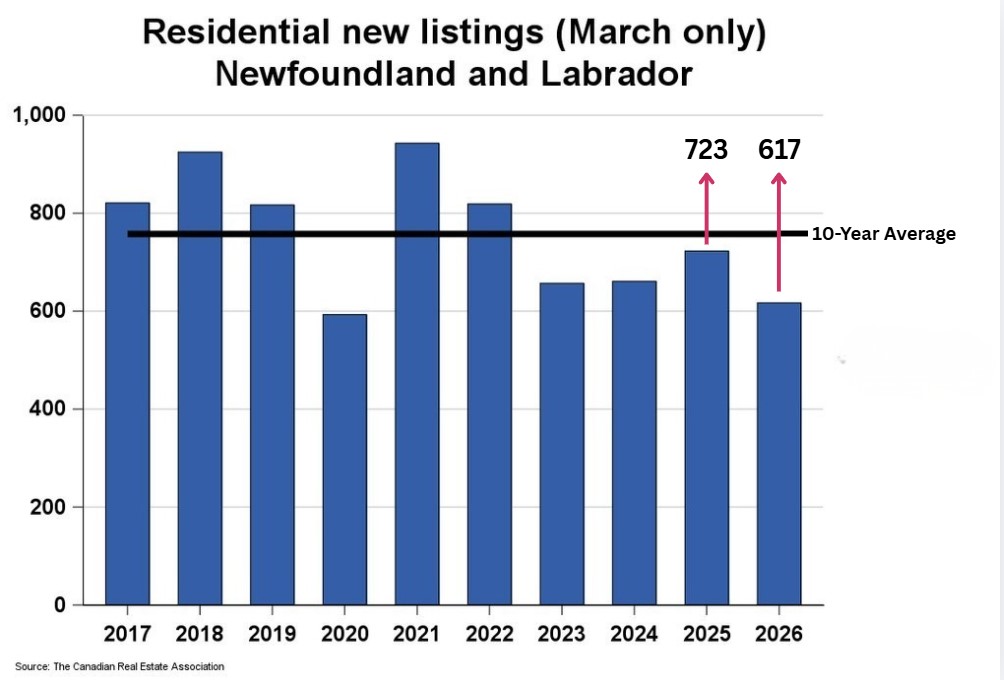

Thee were 617 new residential listing in March 2026, a substantial decrease of 14.7% from March 2025. This was the lowest number of new listings added in the month of March in more than five years.

New listings were 11.3% below the five-year average and 18.6% below the 10-year average for the month of March.

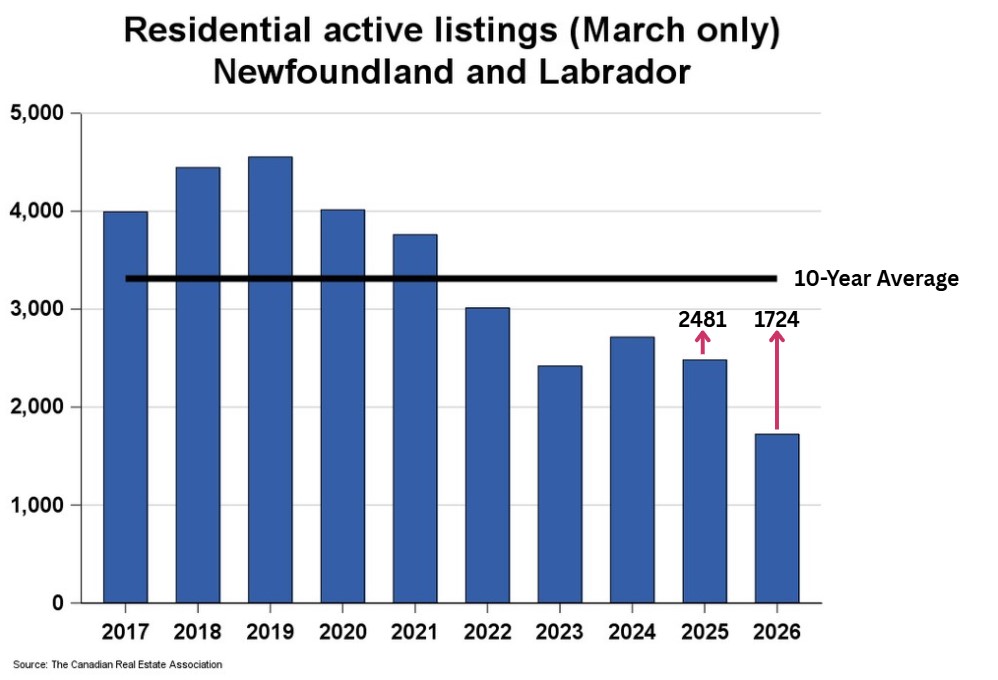

Active Listings:

There were 1724 active residential listings on the market at the end of March 2026, a huge decline of 30.5% from the end of March 2025.

Active listings haven’t been this low in the month of March in more than two decades.

Active listings were 30.2% below the five-year average and 48% below the 10-year average for the month of March.

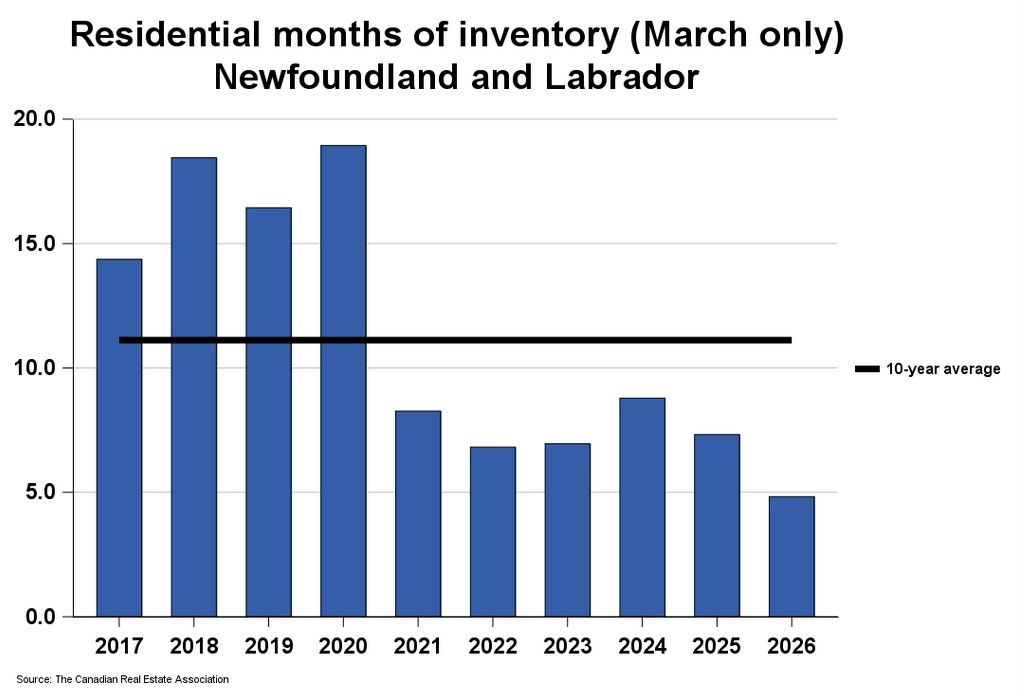

Months of Inventory:

There were 4.8 months of inventory at the end of March 2026, down from the 7.3 months at the end of March 2025 and below the long-run average of 11.1 months for this time of year.

The number of months of inventory is the number of months it would take to sell current inventories at the current rate of sales activity.

Month-Over-Month Comparison For 2026

| Month | Sales | Average Price | New Listings | Number of Active Listings | Months of Inventory at Month End* |

|---|---|---|---|---|---|

| January | 288 | $348,366 | 524 | 1688 | 5.8 |

| February | 272 | $332,983 | 449 | 1665 | 6.1 |

| March | 357 | $352,854 | 617 | 1724 | 4.8 |

*Months of Inventory at the end of each month is calculated by dividing the number of active listings at the end of each month by the number of sales during the month.

This post has been brought to you by:

Gar Mouland, CPA

Canadian Commercial Network of Realtors® (CCN)

Broker/Owner/Operator

Outlier NL Realty

(709) 728-2212

https://www.outliernlrealty.com/

Where great service and great savings happily coexist!

How much is your residential or commercial property/business worth?

Reach out to me at any time for an absolutely free consultation.

Understanding the MLS® Home Price Index (HPI)*

*The MLS® Home Price Index (HPI) is one of the most reliable tools for tracking changes in home prices over time. Unlike average or median sale prices, which can fluctuate sharply from month to month, the HPI provides a clearer picture of true market trends

It tracks price changes for major housing types, including single-family homes, townhouses, and apartments. Prices are measured relative to a base period, making it easy to see how values have risen or fallen over time.

Average and median prices can be misleading because they are heavily influenced by the types of homes sold in a given month.

For example, a rise in luxury home sales can push the average price higher even if typical home values remain unchanged. The MLS® HPI avoids this issue by comparing similar homes over time — an approach often described as an “apples-to-apples” comparison.

Rather than focusing solely on sale prices, the HPI measures how buyers value individual home features.

These include features such as the number of rooms and bathrooms, square footage, lot size, age of the property, and construction details like flooring, roofing, and foundation type. Because these characteristics change gradually, the index produces more stable and meaningful results.